Purchasing adequate landlord insurance for your investment property is vital if you want to protect your income and maintain long-term financial security. But the coverage to which you’re entitled will depend on the terms and conditions of your policy. or this reason, you must read every part of an insurance policy form before going ahead with a deal.

When comparing insurance deals, it’s a good idea to seek advice from an expert. While some insurance providers may appear to offer irresistibly cheap rates, they may not deliver the full coverage you need to protect yourself from all eventualities. A financial expert or insurance agent will quickly spot any holes in an insurance policy and ensure you don't lose money unnecessarily. Of course, it’s also a good idea to learn as much as possible about the insurance landscape. That will ensure you’re well-equipped to engage with insurers and make decisions that work for you.

Related Reading: How to Lower the Cost of Landlord Insurance

What do insurance policies include?

One of the first things to understand about insurance policies is that they come with seven key components, including:

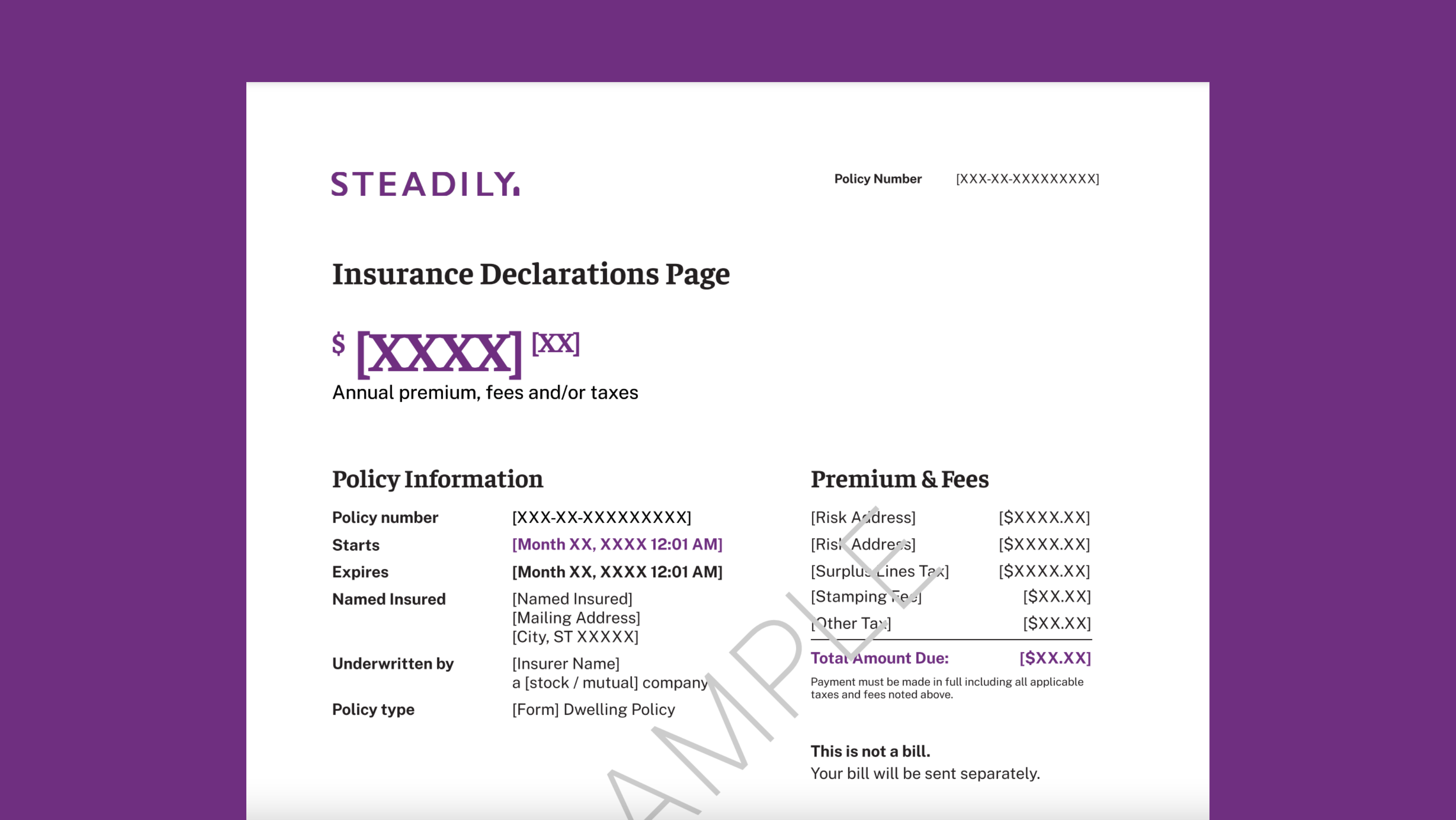

- Declarations: Declarations appear on the first page(s) of your policy and specify the name of the person to whom the insurance applies, the relevant policy address, a summary of the policy, policy limits, and other vital points of information.

- Insuring agreements: This part of the policy outlines who, what, and how the insurance provider is insuring the client.

- Definitions: The definitions page clarifies any key industry terms used in the policy.

- Coverages: This section states the amount of risk or liability protected under the insurance policy, including which items or parts of the property the policy covers.

- Exclusions: Insurance companies provide a section on exclusions to clarify what your policy does not cover.

- Conditions: The conditions of your policy lay out the circumstances under which coverages apply.

- Endorsements: Also known as an addendum, an endorsement refers to an amendment to a policy document.

Key questions to ask about your insurance policy

Before you purchase an insurance policy form, you must ask yourself a few vital questions. These include:

1. Is it a named peril or an open peril policy?

Named peril policies only cover events explicitly listed in the policy form. There are two categories of named peril policies — basic and broad.

Basic named peril insurance policies cover the following:

- Fire

- Lightning

- Storms or hail

- Explosions

- Smoke damage

- Damage caused by aircraft or vehicles

- Riots or civil unrest

- Vandalism or malicious damage

- Leaks caused by sprinklers

- Sinkhole collapse

- Volcanic activity

Broad-named perils policies include additional protection areas on top of the basic form policies, including:

- Burglary

- Fallen objects

- Ice or snow

- Frozen plumbing

- Accidental water damage

- Electricity

Open peril policies, offer coverage for losses linked to perils that are not explicitly ruled out by the policy. Such policies are often more expensive than named peril coverage, but provide better protection. Basic vs broad coverages will vary from carrier to carrier.

2. Does your policy offer replacement cost or actual cash value coverage?

If your insurer provides replacement cost value (RCV) for damaged items, they’ll reimburse you for the amount needed to replace the item, without taking depreciation into account. If they offer actual cash value (ACV) you’ll only receive the value of the property at the time the loss occurred. Broadly speaking, RCV is a superior form of insurance for property owners.

Each policy addresses ACV or RCV for dwelling coverage separately from personal property, i.e., if a customer wants RCV on both the dwelling and contents, they need to check how both are addressed in the policy.

3. Are flood and earthquake coverage excluded?

Insurance policies often exclude damages caused by floods and earthquakes. If your landlord insurance doesn’t cover floods or earthquakes, you’ll need to take out a separate policy — particularly if you live in an area prone to flooding or seismic activity. You may also be able to add flood and earthquake coverage as endorsements on your existing policy, although this will depend on your insurance carrier’s policies.

4. Are your defense costs outside the limit of liability?

Insurance claims sometimes come with a range of defense costs, including lawyer fees, costs of expert witnesses, court costs, and fees associated with filing legal papers. Why? Well, insurance claims are not always clear-cut, and you may need to demonstrate that you are not liable for the damages in question. Defense costs can quickly add up, potentially threatening your reimbursements.

If your defense costs are inside the limit of liability, they’ll be the first expenses deducted from your policy limit when you want to make a claim. If your defense costs are outside the limit of liability, then your insurer offers separate limits or even unlimited funds for defense costs. In such a case, your defense expenses will not erode the sum total of your final settlement. Obviously, you should try to obtain coverage that provides defense costs outside the limit of liability. You may wish to consider taking out liability insurance, which transfers the burden of financial losses due to liability claims from the insured and onto the insurance provider.

Related Reading: What is the Average Cash Flow on a Rental Property

5. What kind of water damage does your policy cover?

Water damage represents one of the most common (and most costly) insurance claims by property owners. However, identifying and claiming for water damage is a little more complex than you might expect. While your policy may cover one type of water damage, it may not cover another type. Most property and homeowners’ insurance policies cover the following types of water damage:

- Water damage after a fire: Most insurers will cover damage caused by the water used to extinguish flames, such as water from a hose or sprinkler system.

- Accidental leaks: These include leaks from appliances or faulty plumbing.

- Burst pipes: Insurers typically cover burst pipes caused by very cold weather. However, they will not cover bursts caused by neglect of the property and insufficient heating.

- Roof leaks: Your policy is likely to cover water damage caused by severe storms or fallen trees. However, you’ll need to be proactive about fixing the roof quickly, or you won’t receive coverage for further water damage.

- Ice dams: You may be eligible to claim for ice dams that form in your gutter quickly and damage your home. However, this claim may be void if poor maintenance caused the damage.

As mentioned, a standard property insurance package is very unlikely to cover flood damage, including damage from tsunamis, storm surges, hurricanes, very heavy rain, and rivers that have burst their banks. If you live in a flood-prone area, you’ll need specialized flood insurance. Other types of water damage your policy is unlikely to cover include:

- Water damage caused by leaks through a foundation.

- Cost of broken appliances: While you may receive compensation for water damage caused by a faulty washing machine, you cannot claim the cost of the washing machine itself.

- Water damage caused by negligence: Failure to address plumbing issues when they arise will harm your claim.

- Water damage caused by earthquakes.

- Water damage related to backed-up sewers or drains: If you’re worried about this problem, you may need to purchase tailored coverage. This is typically available via endorsement to the standard landlord policy and varies by carrier.

- Water damage caused by a sump pump fault.

6. Will your insurer change your roof coverage when it reaches a certain age?

Some insurance providers alter roof coverage when the roof in question reaches a certain age. At this point, they change the reimbursement terms from replacement cost value to actual cash value. Whether or not this applies to your policy will depend on your state. For example, Texas insurers are stricter about insuring older roofs at replacement cost given the frequent and severe hail and thunderstorms in the state.

In fact, it’s worth considering the location of a property and the age of its roof before making an investment. Roof costs could represent a significant cause of profit losses if you’re not careful and fail to pay attention to your insurance exclusion. Other exclusions include cosmetic damage that doesn’t affect the roof’s functionality.

Conclusion

While reading insurance policy forms may not sound like a thrilling activity, it’s a vital part of protecting your investment property. Without adequate coverage, you may suffer losses that jeopardizes your finances and put your tenants at risk.