Landlord insurance policies usually cost about 25% more than homeowners insurance policies, according to the Insurance Information Institute. The average cost of landlord insurance was $1,478 in annual premium, and the average cost of homeowners insurance was $1,192, as of a few years back.

Real numbers depend on the property. For example, we got insurance quotes for a typical 3-unit Chicago rental property from five different companies, and the insurance premiums ranged from $2,400 up to $6,600 for the same coverage.

Steadily's landlord insurance calculator produces a per-policy estimate from your address, year built, and coverage details. Once you've gotten an estimate, you can get a free landlord insurance quote from Steadily today to see how much you can save.

Why does landlord insurance cost more than homeowners insurance?

The main reason for the difference becomes clear when you think about who lives in the home. Insurance carriers see fewer claims and lower average loss amounts in owner-occupied homes than rentals. Common sense says no one will take care of a property quite like the owner.

And another difference shows up when you look at the amount of liability insurance coverage. Landlords have higher coverage levels to protect themselves from lawsuits and legal fees that arise from injured tenants or guests. It's normal for a landlord policy to have a $1m liability limit.

Are there landlord insurance discounts?

Discounts exist, but it's not as deal-driven as other types of coverage like car insurance. For instance, State Farm grants price breaks for good grades or driving courses. You won't find anything like that with landlord insurance.

Instead, take a glance at these two ways to save:

- Safety Devices. Install burglar alarms, fire sprinkler systems, or motion sensors to drive down the price.

- Multiple Properties. Bundle landlord insurance for all your rentals with the same company to lower your premium on each policy.

Does my homeowner's insurance policy cover my rental property?

It depends. Answer how often you rent the property and how long people stay to decide what type of insurance you need. Check out these three scenarios to help you pick:

- Frequent Short-Term Rentals. For Airbnb, VRBO, or another setup where various guests stay for a brief time like a bed-and-breakfast or hotel, you'll need a commercial insurance policy.

- Infrequent Short-Term Rentals. For rentals of your primary residence for less than 30 days, for example, while you take a vacation, you may use your homeowners policy with your insurance provider's approval.

- Long-Term Rentals. For periods beyond short-term, such as a typical 6-month or 1-year lease, you should buy a landlord policy.

A general rule to help, personal insurance doesn't cover commercial activity. For instance, many personal finance experts suggest an umbrella policy to protect you from liability claims above your homeowner's policy limits. But your umbrella policy would not apply to your rental investment property if you set it up as a separate business or LLC.

Curious about insuring your property? Get a quote in seconds:

Should I also buy renters insurance?

No, you need not buy both a landlord policy and a renters policy. Some confusion comes from the fact that landlord insurance is sometimes called rental property insurance. Rental property insurance policies cover houses, and renters insurance policies protect your tenants' personal belongings and liability.

Many landlords require their tenants to buy renters insurance because it reduces headaches when personal property claims arise. For example, if a fire damages your rental and destroys your tenants' property, they may seek damages against you even though they should have safeguarded themselves with a renters policy.

And landlords request tenants buy renters insurance to protect the tenants after a major claim. Let’s go back to the fire example. If the tenant had to move until repairs were finished, how would they pay for living expenses? The renter's policy would cover that for them, while your landlord insurance compensated you for your loss of rental income while the home is made livable.

A real-world landlord insurance example

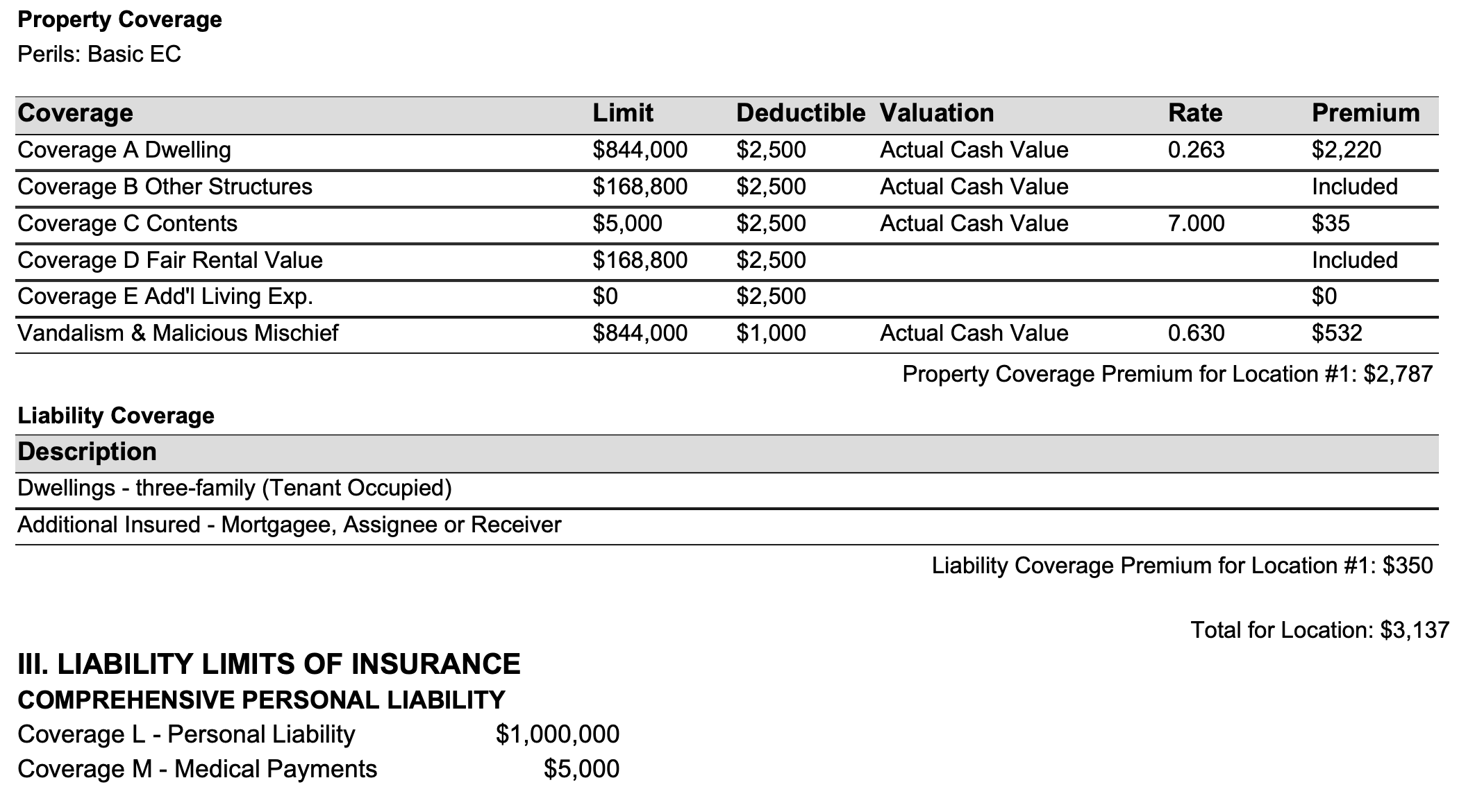

Let's look at a real rental property to break down what kind of insurance coverage it has and the costs. This 3,700 square-foot apartment building with three rental units lies near downtown Chicago on Fullerton Avenue. It last sold for $950,000 in 2018, and the owner thinks its replacement cost would be about $740,000 at $200 per square foot. It's fully rented and bringing in a monthly rental income of $6,000.

The owner got three quotes from his insurance agent and bought the landlord insurance policy from USLI for a total annual premium of $3,137.

First, let's review his insurance coverage and then break down what it means.

- Dwelling: $844,000 limit, $2,500 deductible

- Other structures: $168,000 limit

- Contents (personal property): $5,000 limit

- Fair rental value: $168,800 limit

- Vandalism: $844,000 limit

- Personal liability coverage: $1,000,000 limit

- Medical payments: $5,000 limit

Looking at the cost of each line item, we see that some are much more expensive than others:

- Dwelling: $2,200 annual premium

- Contents: $35 annual premium

- Vandalism: $532 annual premium

- Liability coverage: $350 annual premium

The dwelling coverage would pay to rebuild the entire building if there were extensive property damage from a fire or natural disaster, so it makes sense that this coverage is the most expensive part at $2,200.

Moving on to "contents," this will cover damage to the landlord's personal property that's kept at the rental property. It's important to note that this does not protect the tenants' personal property — that's what a renters insurance policy is for. Because the limit here is only $5,000, the insurance company isn't taking on much risk, so the coverage only costs $35.

Next up is vandalism coverage. This insurance coverage is quite pricey at $532. This real estate sits in a dense urban area, which drives up the risk and cost of this additional coverage.

Last, the liability insurance costs $350 for $1m in liability protection and $5,000 in medical payments for tenants and their guests. Liability is one of the factors included in what landlord insurance costs.

What's wrong with this example

The owner believes that his landlord insurance coverage protects against just about anything that could happen to his property, and he's in good shape. He's not.

Did you notice the column in the printout where it says "Valuation?" There you'll find the words "Actual Cash Value." That doesn't mean what it sounds like.

Actual Cash Value (ACV) is what someone would pay you in cash for a piece of property: the replacement cost minus depreciation. For instance, let's say the owner installed a roof, and it costs $40,000—that's the replacement cost. But he installed the roof in 1999, so by now, it's racked up $18,000 in depreciation. The Actual Cash Value is now only $22,000; that's the replacement cost of $40k minus $18k in depreciation.

So, if the landlord has a covered loss on the roof, his property coverage will only value the roof at $22,000, even though it will cost $40,000 to repair. It gets worse. The owner has a deductible of $2,500. Finally, the owner will end up with a check for only $19,500 to replace a roof that will cost $40k. That means he must come up with $20,500 out of pocket.

Bottom line: The owner should probably get a new quote where the valuation method is "Replacement Cost" instead of "Actual Cash Value." These two factors influence landlord insurance costs.

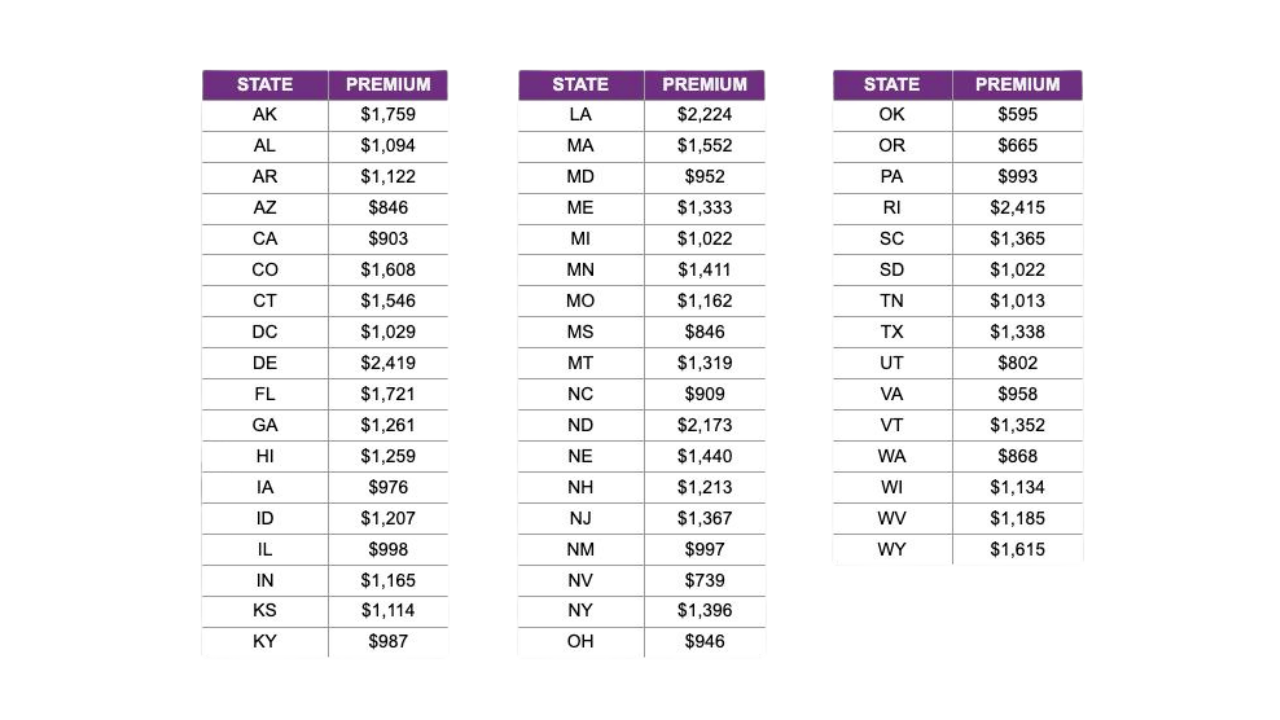

How much does landlord insurance cost in each state?

While the average cost of landlord insurance across the nation is approximately $1,478 annually, it's essential to consider regional variations. In some states, the average cost might be higher or lower than the national average due to factors like property values, local regulations, and risk factors. For instance, states with a higher risk of natural disasters or higher property values may experience higher landlord insurance costs. To get a comprehensive understanding of the average landlord insurance cost in each state, you can refer to our interactive map, below, or state-by-state overview here.

Cost by coverage tier

State average is one part of the cost picture. The other is how much dwelling coverage you carry. Premium scales roughly with the rebuild cost the policy is insuring, so a $100,000 dwelling and a $1 million dwelling on otherwise identical properties produce very different annual numbers. State-level averages also fold in the full range of coverage tiers and policy types, which is why Steadily quote data shows averages running from around $892 per year in low-risk states like Idaho up to $2,561 per year in Louisiana. Below are typical premium ranges for the four most common coverage tiers, holding state and property details to typical levels.

$100,000 dwelling coverage

A $100,000 landlord insurance policy typically costs around $500 to $1,000 per year on a DP-3 special form, though state and property factors move the number up or down. This tier usually fits older homes, smaller condos, manufactured homes, properties bought below current rebuild cost, and rentals in markets where construction prices run low. The tradeoff is real: $100,000 sits below the rebuild cost of most U.S. single-family rentals, which exposes the landlord to coinsurance penalties or out-of-pocket gaps if a total loss happens. Carriers may also cap loss of rent, liability sub-limits, and certain peril coverages on lower-value policies. Before settling on this tier, check that the figure actually matches what it would cost to rebuild the structure today, not what you paid for the property. Insurance pays based on rebuild cost, not market price, so a $100,000 tier on a property that would cost $200,000 to rebuild leaves real exposure. The Steadily landlord insurance calculator produces a property-specific estimate at this tier using address-level data rather than state-wide averages.

$300,000 dwelling coverage

The $300,000 tier is the most common landlord insurance setting in the U.S., typically running between $900 and $1,800 per year for a DP-3 policy on a standard single-family rental. The number represents a roughly accurate rebuild cost for most three-bedroom homes outside high-rebuild-cost metros, which is why most carriers default new quotes to something near this tier. Premium within the $300,000 range is driven by state-level peril exposure (hurricanes in coastal markets, wildfire in California and the West, hail in the Plains), property age and roof condition, fire protection class, and claims history. Loss of rent coverage on a $300,000 dwelling typically caps at 12 months of fair rental value, which works out to between $20,000 and $40,000 of additional coverage depending on the local rent market. For most landlords with a single-family rental in a mid-tier rebuild market, this is the tier where coverage is genuinely matched to risk. Property-specific quotes at this tier come out of the Steadily landlord insurance cost estimator.

$500,000 dwelling coverage

The $500,000 tier typically costs between $1,400 and $2,800 per year for a DP-3 policy, with the wider range reflecting larger gaps between low-risk inland states and high-risk coastal or wildfire markets. This tier suits properties in higher-cost metros (Bay Area, NYC outer boroughs, Boston, Seattle), newer construction with finished basements or premium materials, and homes with rebuild estimates pushed up by labor or material constraints. A $500,000 policy is also where the math starts to favor adding ordinance-or-law coverage and an umbrella policy, since the value at risk is large enough that older building codes and big liability claims can produce out-of-pocket gaps the standard policy doesn't fill. Loss of rent coverage scales up at this tier to often $40,000 to $60,000 of additional protection. For coastal Florida or Louisiana properties at $500,000 dwelling value, premium can run $3,000 or more per year due to named-storm exposure, which is why state averages on the high end already push $2,400 to $2,561 across all tiers. The landlord insurance calculator produces a tier-specific quote that accounts for those state-level cost drivers.

$1,000,000+ dwelling coverage

Policies with $1,000,000 or higher dwelling coverage typically run $2,500 to $5,000+ per year, though the upper bound stretches well past that for true luxury properties in high-cost or high-risk markets. This tier covers larger luxury rentals, multi-family buildings written as DP-3 (smaller multifamily fits under personal landlord policies; larger ones move to commercial property forms), and properties where rebuild cost reaches or exceeds seven figures due to size, finish quality, or location. At this dwelling value, sub-limits on the standard policy often need to be increased separately: liability is usually written at $1 million as a ceiling on the base policy, with umbrella commonly added for an additional $1 million to $5 million of liability protection. Loss of rent at this tier can reach $80,000 to $150,000 in coverage, reflecting the higher rents these properties typically command. A property-specific quote at this tier usually requires a guided conversation with an underwriter rather than a standard online flow, but Steadily's landlord insurance estimator produces an initial number based on the dwelling and location details.

Factors that influence the cost of landlord insurance

Regional variation in risk profiles significantly impacts the cost of landlord insurance in each state. Insurance companies assess risk based on various factors specific to a region, such as:

- Natural Disasters: States prone to hurricanes, earthquakes, tornadoes, wildfires, or floods are considered high-risk for property damage. Insurance companies will charge higher premiums in these regions to offset potential losses from natural disasters.

- Crime Rates: Areas with higher crime rates may experience increased risks of property damage or theft, leading to higher insurance costs.

- Property Values: States with higher property values will generally have higher insurance costs, as it will cost more to rebuild or repair a property in the event of a loss.

- Building Age and Condition: Older buildings may have higher insurance costs due to a higher likelihood of wear and tear, leading to potential maintenance issues.

- Tenant Characteristics: The type of tenants and their occupancy behavior can influence insurance rates. For example, student rentals or short-term rentals like Airbnb might be considered higher risk.

- Laws and Regulations: State-specific regulations and laws regarding landlord-tenant relationships can also impact insurance costs. For example, states with tenant-friendly laws may lead to higher liability risks for landlords, affecting premiums.

- Claims History: The frequency and severity of insurance claims in a particular region can affect insurance costs. Areas with a history of frequent claims may have higher premiums.

- Available Coverage Options: Different states may offer different coverage options and endorsements, which can affect overall insurance costs.

Due to these regional variations in risk profiles, landlord insurance costs can vary significantly from state to state. Landlords in high-risk areas can expect to pay higher premiums to protect against potential losses, while those in low-risk regions may enjoy more affordable insurance rates. It's crucial for landlords to understand the specific risk factors in their area and work with insurance providers who specialize in coverage tailored to their region's needs. Shopping around and comparing quotes from different insurers can also help landlords find the most competitive rates for their specific location and property type.

Landlord insurance options by state

- Landlord Insurance In Arizona

- Landlord Insurance In California

- Landlord Insurance In Kansas

- Landlord Insurance In Texas

- Landlord Insurance In Georgia

A tip for future landlords

We spoke with a real estate investor and he shared an insight on how he uses landlord insurance for the properties that he rehabilitates that he rents out to tenants in the future.

Remember you should only have a landlord insurance policy in place when the property is actually tenant occupied. You need what is called a vacant policy which as you can imagine is more expensive because statistically, a vacant property is much more likely to file a claim. We use a vacant policy after we have completed construction and are waiting to place a tenant. After the tenant has moved in we convert the policy to a landlord policy which is cheaper. Looking back at your historical expenses a vacant policy is 120% more expensive than a landlord policy (861 annual landlord versus 1880 annual vacant)

Bill Samuel | Blue Ladder Development